HubLab Notes:

In March 2011, I provided a HubLab with social enterprise attorney, Inder Comar at San Francisco's Hub. HubLabs are workshops for social entrepreneurs who are members of the Impact Hub, a global network of shared work places where social entrepreneurs go to work. These are the notes from our session. Hope this resources help others trying to decide whether to be for-profit or not-for-profit!

My usual disclaimer:

'I am trained in the law, but I am not a lawyer.

Nothing that I say should be considered legal advice.

Please consult with a real lawyer.'

Following which, people usually respond:

'gosh, you sure sound like a lawyer.'

Key considerations when determining a corporate structure:

Purpose: Structure needs to align with the enterprise’s mission. Consider whether flexibility to adapt to changing conditions is important.

Method: Structure may shape, support and/or limit the enterprises’ activities. Consider how structure influences the enterprise’s ability to fulfill its purpose.

Funding: Structure needs to suit the investor/funding needs of the entity

Growth: Structure needs to support growth/scale to achieve the operating goals of the enterprise.

Tax: Structure needs to optimize taxes both for the venture and for the funders/donors.

IP: Structure may need to support IP ownership

Location: Corporate laws are state based. Consider what state has the most advantageous corporate law for your enterprise based upon what, where and how the venture will fulfill its mission.

Risk tolerance/Accountability: Structure determines control and accountability. Consider governance and stakeholder interests. Newer legal structures are not legally “tested,” creating more uncertainty for an enterprise.

Location: Corporate laws are state based. Consider what state has the most advantageous corporate law for your enterprise based upon what, where and how the venture will fulfill its mission.

Liability: Structure may influence one’s eligibility for insurance and likelihood of litigation. Consider how structure will influence employment obligations and human resources.

Costs: Structures have different legal and administrative costs at the outset and related to ongoing maintenance. Consideration of the benefits of the structure should include evaluation of the resources necessary to create and maintain the entity and the potential barriers/costs associated with the need for potential structural changes at a future time.

Purpose: Structure needs to align with the enterprise’s mission. Consider whether flexibility to adapt to changing conditions is important.

Method: Structure may shape, support and/or limit the enterprises’ activities. Consider how structure influences the enterprise’s ability to fulfill its purpose.

Funding: Structure needs to suit the investor/funding needs of the entity

Growth: Structure needs to support growth/scale to achieve the operating goals of the enterprise.

Tax: Structure needs to optimize taxes both for the venture and for the funders/donors.

IP: Structure may need to support IP ownership

Location: Corporate laws are state based. Consider what state has the most advantageous corporate law for your enterprise based upon what, where and how the venture will fulfill its mission.

Risk tolerance/Accountability: Structure determines control and accountability. Consider governance and stakeholder interests. Newer legal structures are not legally “tested,” creating more uncertainty for an enterprise.

Location: Corporate laws are state based. Consider what state has the most advantageous corporate law for your enterprise based upon what, where and how the venture will fulfill its mission.

Liability: Structure may influence one’s eligibility for insurance and likelihood of litigation. Consider how structure will influence employment obligations and human resources.

Costs: Structures have different legal and administrative costs at the outset and related to ongoing maintenance. Consideration of the benefits of the structure should include evaluation of the resources necessary to create and maintain the entity and the potential barriers/costs associated with the need for potential structural changes at a future time.

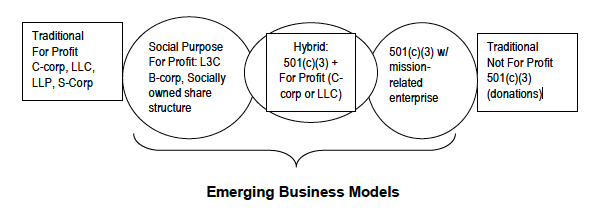

Spectrum of Emerging Business Models

Traditional Structures: Accounting firms often produce good overviews of tax implications and value of different business structures:

* Non-Profit 501(c)(3): charitable purpose, tax exempt not for profit organization

* Sole proprietorships (bulk of business run by individuals where personal liability is low - think flower shops)

* LLCs (cheap to file, flexibility in allocating profits and losses)

* S-corps (just like a publicly traded-firm but with a cap on the number of shareholders - e.g. dozens, not millions)

* C-corps (expensive to maintain and really only helpful if you want a global company that is going to launch on a stock exchange).

Emerging Business Models

LC3: social charitable mission + limited liability corporation

B-Corp: social/charitable mission + full corp tasked with balancing social/env/profit (more expensive, better for large ventures expecting large investment capital)

Hybrids:

A) Non-profits w/ For-Profit Subsidiary (Taproot) --> for generating revenue for NP parent *tricky due to the potential for unrelated earned income to jeopardize non-profit status http://www.sdlaw.com/files/Download/subsidiaries.htm

B) For-Profit with NP-Foundation (Google/McKesson) --> for dispersing revenue For a thorough review of advantages and disadvantages for each type on this continuum, please see: Fruchterman, J. For Love or Lucre, Stanford Social Innovation Review, Spring 2011, p. 42-47.

Traditional Structures: Accounting firms often produce good overviews of tax implications and value of different business structures:

* Non-Profit 501(c)(3): charitable purpose, tax exempt not for profit organization

* Sole proprietorships (bulk of business run by individuals where personal liability is low - think flower shops)

* LLCs (cheap to file, flexibility in allocating profits and losses)

* S-corps (just like a publicly traded-firm but with a cap on the number of shareholders - e.g. dozens, not millions)

* C-corps (expensive to maintain and really only helpful if you want a global company that is going to launch on a stock exchange).

Emerging Business Models

LC3: social charitable mission + limited liability corporation

B-Corp: social/charitable mission + full corp tasked with balancing social/env/profit (more expensive, better for large ventures expecting large investment capital)

Hybrids:

A) Non-profits w/ For-Profit Subsidiary (Taproot) --> for generating revenue for NP parent *tricky due to the potential for unrelated earned income to jeopardize non-profit status http://www.sdlaw.com/files/Download/subsidiaries.htm

B) For-Profit with NP-Foundation (Google/McKesson) --> for dispersing revenue For a thorough review of advantages and disadvantages for each type on this continuum, please see: Fruchterman, J. For Love or Lucre, Stanford Social Innovation Review, Spring 2011, p. 42-47.

In "For Love or Lucre", Benetech founder Jim Fruchterman proposes these 4 questions:

• What are your motivations for starting the venture?

• What market are you targeting?

• How do you plan to raise capital?

• What type of control do you want over the venture?

• What are your motivations for starting the venture?

• What market are you targeting?

• How do you plan to raise capital?

• What type of control do you want over the venture?

RSS Feed

RSS Feed